According to the Australian Bureau of Statistics, Australians lost a staggering $2.2 billion to card fraud in 2023. And while consumers are becoming more scam-savvy, it’s still vital you take every step to protect your business – and your customers.

One easy way to do that?

With 3D Secure – an additional security layer designed to make online transactions safer. But what is it exactly, and how does it work?

Read on to find out.

What is 3D Secure?

3D Secure (3DS) is a security protocol that adds an extra layer of protection to online credit and debit transactions.

Designed to reduce the risk of unauthorised transactions and fraudulent activities, 3DS broadly involves a 3-part verification process with the card issuer, the merchant (that’s you) and the cardholder.

You may already know 3DS by its other branded names: Visa Secure, Mastercard Identity Check, and Diners Club ProtectBuy.

How does 3DS work?

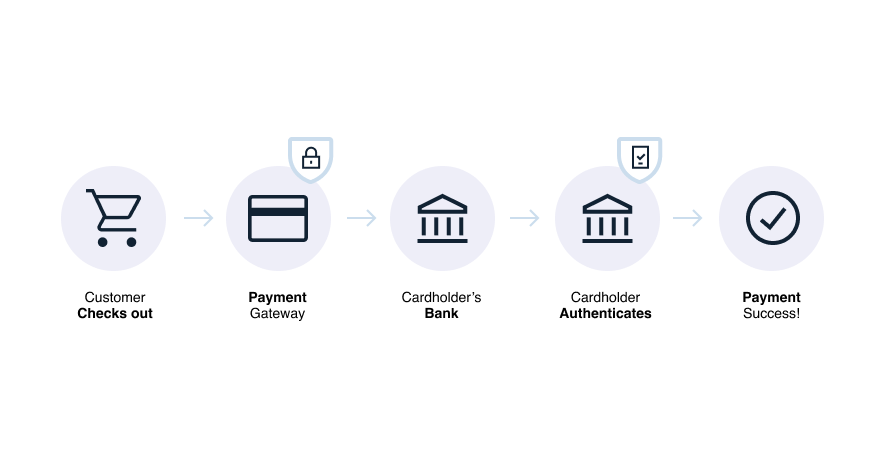

Here’s an example of how 3DS works when your customer makes a purchase:

- The customer makes an online purchase.

- Your payment provider sends the data to the cardholder’s bank to verify the transaction.

- The bank either approves the transaction OR decides that further authentication is needed.

- If further authentication is needed, the cardholder must enter a one-time password or complete biometric authentication—like fingerprint or facial recognition—via their banking app.

- Once authentication is received, the transaction is complete.

3DS: A more secure way to pay

If your business accepts online transactions, we recommend using 3DS as an additional tool to mitigate fraud risk on high-value transactions. This will allow you to:

- Secure high-risk transactions. For transactions with high value or higher fraud risk, such as international transactions, 3DS provides that extra layer of protection – and peace of mind.

- Lower the risk of losses. By verifying the cardholder’s identity, 3DS can help prevent unauthorised transactions. This reduces the risk of losses and costs associated with chargebacks and fraud.

- Protect your business. If you use 3DS – and the transaction is successfully verified – the liability for a fraudulent transaction generally remains with the card issuer or bank. But without 3DS, your business could be liable.

- Increase customer confidence. By implementing 3DS, you show your customers that you’re committed to their security. This helps them feel more comfortable buying from you this time – and the next.

When not to use 3DS

While 3DS adds an extra layer of protection, it does come with some disadvantages. Namely, the potential friction to the checkout process.

Consider these factors before deciding if 3DS is the right choice for your business:

- It’s unnecessary for low-risk transactions: 3DS adds an extra step to the checkout process, which may not be ideal for low-value, low-risk transactions. For example, having to complete another authentication just to pay for a $20 membership payment may annoy your customers – and cause them to abandon payment.

- It may cause a less seamless checkout experience: Some customers – especially those making impulse purchases – may find the additional authentication step cumbersome. Once again, this could lead to a higher rate of cart abandonment.

Pin Payments: Your 3DS partner

At Pin Payments, we’re serious about helping you protect your customers. So we enable 3DS for all charges that are processed through:

If your business has more complex needs – you can enable 3DS via our Charges API. Check out our 3DS integration guide for more details.